Eliminating debt is just that simple!

It never ceases to amaze me how people seem to just amass mountains of debt, and the ‘creative reasons’ they list for having done so. From the instant gratification of “gotta have it now!”, to keeping up with the Joneses, or just the insidious swipe of the credit card to pay for our morning coffee on the way to work. Americans seem to have every excuse in the book for why they are in debt, and it’s always ‘not their fault’. Now don’t get me wrong, emergencies do happen, and tragedies do occur, always at the worst possible time and in the most expensive manner. Grabbing breakfast and a coffee on the way to work is NOT an emergency. A new bigger HDTV is NOT an emergency. A new outfit when you have a wardrobe bursting with unworn clothes is NOT an emergency. These are bad habits that you’ve fallen into and the credit card which has allowed you to charge up this mountain of debt was your responsibility.

NO NEW DEBT!

When I found myself in $50,000 worth of debt in 2001, I thought I’d never crawl out of the hole I had dug myself into. It took years of hard work and discipline to become debt free, and I was ridiculed by several know-it-alls who could not comprehend why I just didn’t file for bankruptcy and make it ‘easy’ on myself. Often times, the ‘easy way’ is the wrong way. Bankruptcy is FOREVER. And if you refuse to change your behavior, you’ll find yourself back in the same situation as before. I’ve witnessed friends making the same mistakes after filing bankruptcy. Because THEY refused to alter their behavior, their chances of ever becoming debt free are the same as a snowball’s chance in a blast furnace. The first step towards recovery is NO NEW DEBT! You can’t spend one cent on ANYTHING that isn’t essential. Don’t even charge a stick of gum. NOTHING! If you lack the willpower to stop using your credit cards, you MUST cut them up. I remember as a boy watching an old TV show from the late 70’s called WHAT’S HAPPENING!! A character named ReRun (played by Fred Berry) gets his first credit card, and quickly gets into trouble. One credit card quickly turns to a dozen, and soon he needs to finance his credit cards with a loan. In quick order, everything he owns including the Monopoly game and even his red beret gets repossessed. In the penultimate scene of the episode, ReRun and friends sell EVERYTHING in the apartment except his food processor, which he fills with his credit cards to make ‘credit card coleslaw’.

The Debt Snowball

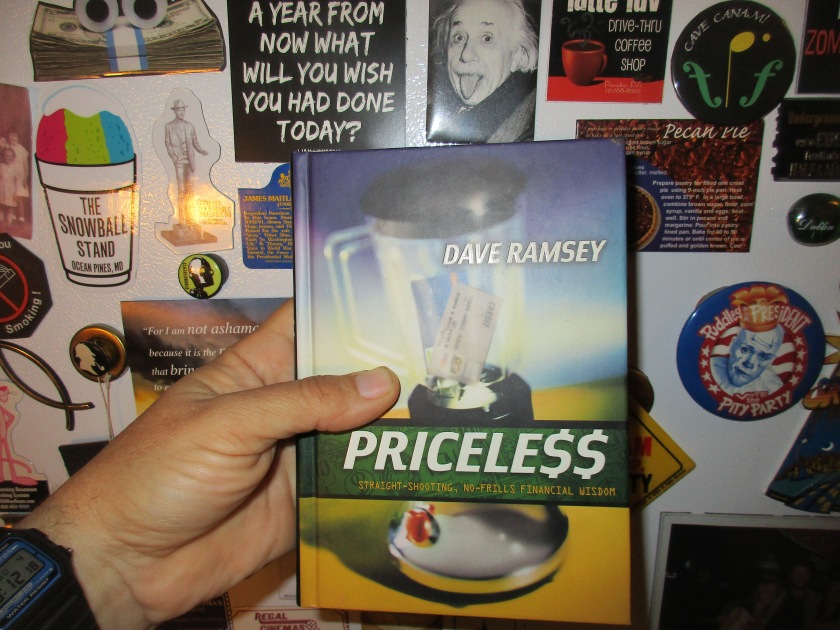

The level of intelligence which created a problem is never sufficient to solve the problem, and that’s why there are walls of self-help books in bookstores. It’s so that you have the ability to consult someone wiser than yourself and find a solution to your problem. For me, that wise counsel came from reading books by Dave Ramsey. While in a discount remainder store, I found a thin book titled Pricele$$ marked down to $2.99. What drew me to the book was the cover depicting credit cards in a blender which reminded me of the What’s Happening!! episode.

While reading his book Pricele$$, I first learned about his debt-destroying weapon, The Debt Snowball. It is the opposite of the more convention debt stacking, or debt avalanche payment method. In the traditional debt stacking method, you pay the bill with the highest interest rate off first. You dump all your extra cash into this bill while maintaining the minimum payments on all other bills. Like an avalanche of money just wiping that debt off the face of the Earth. Dave Ramsey instead advocates the opposite approach, which he dubs ‘The Debt Snowball’. Picture a small snowball rolling downhill increasing in size and speed as it gains momentum. With this method, you list all of your debts in order from smallest to largest regardless of interest rate, and their minimum monthly payment. You then use every extra penny you have to pay off that smallest of your bills first. As soon as you wipe it out, you apply its minimum payment and add it to the minimum payment of the next bill on the list. You repeat this process until all debts are paid. This method worked for me, and it will work for anyone as long as you follow three simple rules.

- No new debt. You can’t charge anything.

- All ‘extra’ money from cutting non-essentials must be used for paying down the smallest debt.

- You MUST keep making the minimum payments on all your bills.

The last one is a real no-brainer. You can’t stop paying one existing bill to finance another. I tell myself that no one could be this stupid, but just this week, a friend-of-a-friend had her car repossessed for non-payment because she needed the car money to save for a down payment on a new apartment. I can’t fathom how she convinced herself that this was a great idea. Like I wrote last week, few (if any) of my friends take my financial advice seriously, often choosing their own disastrous schemes over wise council. Like the old saying goes, “a fool and his money are soon parted.” As always, I wish you happiness and success!