What’s in a name?

(part one of a two-part series on The Federal Reserve Bank.)

‘I wish it were possible to obtain a single amendment to our Constitution. I would be willing to depend on that alone for the reduction of the administration of our government; I mean an additional article taking from the Federal Government the power of borrowing.’– Thomas Jefferson, (from a letter sent to John Taylor on Nov. 26, 1798.)

When most Americans see the word ‘federal’ they automatically associate it with the US FEDERAL Government. By viewing the word as synonym instead of as an adjective, it has led to a confusion of meaning. Adjectives describe persons, places, or things, BUT describing something is not always the same as being something, and there are also subjective as well as objective descriptions which can be led by emotions verses facts. In a very broad example of what I mean, let’s consider the following example: Susie calls Bobby a lazy boy at a birthday party. Her season for the statement was because she didn’t care for the way he wrapped the birthday gift. Does this mean that Bobby IS lazy? Bystanders at the partying overhearing Susie’s statement quickly take sides, some agreeing with Susie, others standing up for Bobby. None of these emotional reactions are proof of the original subjective and possibly slanderous statement made by Susie against Bobby. Yet this seems to be the modern mindset in contemporary society. It’s like calling Trump supporters racists. If you FEEL someone is something, does that automatically make them that thing? If you hear someone else describe something, does that make it the same for you? While some things may be immutable, others can vary widely over time or circumstance, and change from person to person.

If you asked the average person in the USA if the Federal Reserve Bank is part of the Federal Government, they would more than likely say yes, and they would be absolutely wrong.

According to Collins Dictionary of English, the number one definition of Federal is:

- Federal–of or formed by a compact; specif., designating or of a union of states, groups, etc. in which each member agrees to subordinate its governmental power to that of the central authority in certain specified common affairs.

The shipping company FedEx was originally called Federal Express before the company name was shortened in 2000 to its current moniker. The company was founded in 1971 by Frederick W. Smith and is currently the eight-largest private employer in the US. Mr. Smith chose the name because he believed the patriotic meaning associated with the word “federal” suggested an interest in nationwide economic activity. He also hoped the name would resonate with the Federal Reserve Bank, a potential customer.

The Federal Reserve Bank is NOT part of the US government.

The Federal Reserve Bank was the third attempt by representatives of the US Government to create a central banking system to oversee the nation’s financial needs. Unlike its predecessors, this current bank was NOT restricted by a twenty-year charter, and its many economic policies over the past century are directly responsible for the skyrocketing government debt which now exceeds $25.2 trillion. That amounts to over $81,000 per citizen, or $139,000+ per tax payer (Since not all citizens pay taxes.)

A bit of history

The First Bank Of The US

The first secretary of state, Alexander Hamilton was a great admirer of the Bank of England and was pressing President Washington to sign a bill creating the First Bank of the US. Washington had grave misgivings against signing the ‘bank bill’. Thomas Jefferson and James Madison were strongly opposed to the measure. Ultimately, after considering many opinions on the matter, and having decided that the bank bill was constitutional, Washington signed the bill into law on Feb 25th, 1790. The building for the newly created bank was built in Philadelphia in 1791. Twenty years later, In 1811, the U.S. Senate tied on a vote to renew the bank’s charter. Vice President George Clinton broke the tie and voted against renewal, killing the institution.

The Second Bank of the US

Modeled on Alexander Hamilton’s First Bank of the United States, the Second Bank was chartered by President James Madison in 1816 and began operations at its main branch in Philadelphia on January 7, 1817 managing twenty-five branch offices nationwide by 1832. President Andrew Jackson was the seventh president of the US, elected in 1829, was absolutely hated the bank, arguing that the bank was a corrupt institution which failed to produce a stable national currency, was unconstitutional, and was dangerous to American liberties. He managed to convince congress NOT to renew the charter for the bank in 1836. It folded in 1841.

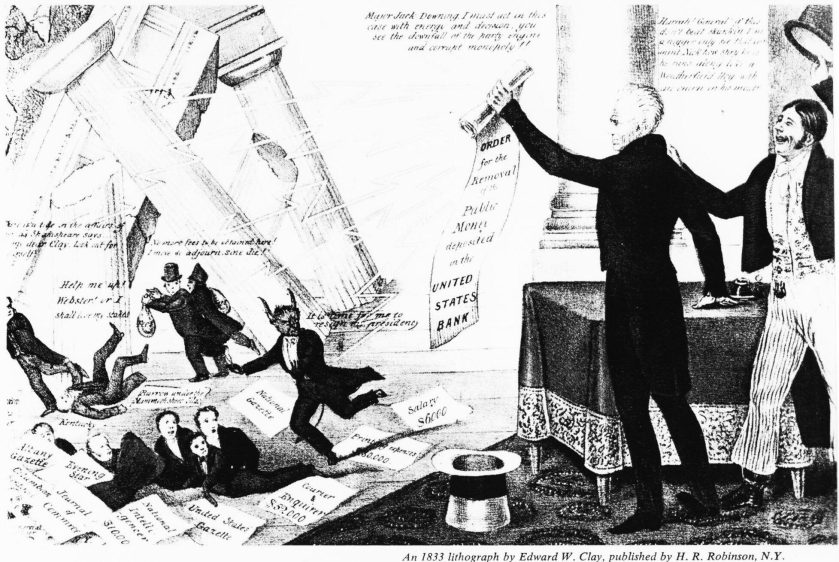

A political cartoon from 1833 shows Jackson destroying the bank with his “Order for the Removal,” to the approval of the Uncle Sam like figure to the right, and the annoyance of the bank’s president, shown as the Devil himself.

“That is to say, under the old way any time we wish to add to the national wealth we are compelled to add to the national debt.

Now, that is what Henry Ford wants to prevent. He thinks it is stupid, and so do I, that for the loan of $30,000,000 of their own money the people of the United States should be compelled to pay $66,000,000 — that is what it amounts to, with interest. People who will not turn a shovelful of dirt nor contribute a pound of material will collect more money from the United States than will the people who supply the material and do the work. That is the terrible thing about interest. In all our great bond issues the interest is always greater than the principal. All of the great public works cost more than twice the actual cost, on that account. Under the present system of doing business we simply add 120 to 150 per cent, to the stated cost.

But here is the point: If our nation can issue a dollar bond, it can issue a dollar bill. The element that makes the bond good makes the bill good. “– Thomas A. Edison

The Federal Reserve Bank

The Federal Reserve Act was signed into law by President Wilson on December 23, 1913. It created and established the Federal Reserve System, the central banking system of the United States. It also gave the newly established system legal authority to issue Federal Reserve Notes (U.S. Dollar). The act had far reaching implications including the internationalization of the U.S. Dollar as a global currency.

Unfortunately the massive downside is that since its creation the Federal Reserve, (or sometimes just called the Fed) is directly responsible for the national debt, and the devaluation of the US dollar of 92%. The money the USA ‘borrows’ from the Fed is money that is ‘created’. They just order the mint to print more money. Then they charge interest on the created money. Currently the US can’t even afford to pay the interest on the money it’s loaned.

The fact of the matter is that the government NEEDS money to run, but it was no way to produce money. You can’t create prosperity by spending yourself into debt. Consider that over the next week, and come back next Sunday for part two of this long blog post on the Federal Reserve Bank. As Always, I wish you success and happiness!