Can the debt ever be repaid?

“A national debt, if it is not excessive, will be to us a national blessing.” – Alexander Hamilton

The average American doesn’t understand how money, budgets, and debt work at the local level. Personal finances are referred to by economists as ‘microeconomics’. When you start dealing with the finances of nations, your discussing what is known as ‘macroeconomics’. In any case, the underlying principals of income, budgeting, and debt are basically the same, only the scale is different. Savings is always good, and debt is never your best choice. Debt in and of itself is just a tool, but it can quickly spiral out of hand, and you are always spending more money when you go into debt than if you were to pay the full amount upfront in cash. The decision that needs to be greatly mulled-over is the benefits of waiting verses the benefits of instant gratification.

Going into debt for any reason is never to be taken lightly, and should NEVER be used for trivial pursuits. Sometimes it can be very important to make an purchase in order to establish a platform for future benefits. On a personal level, an example of this could be purchasing an automobile. There are not many individuals who buy brand new cars outright with cash, though older, used cars might be attainable. In some parts of the USA a car is a necessity. You can’t get to work, or buy groceries because there is no direct public transportation available. Buying items you really don’t need like the latest video game, or the newest smart phone are examples of foolish debt.

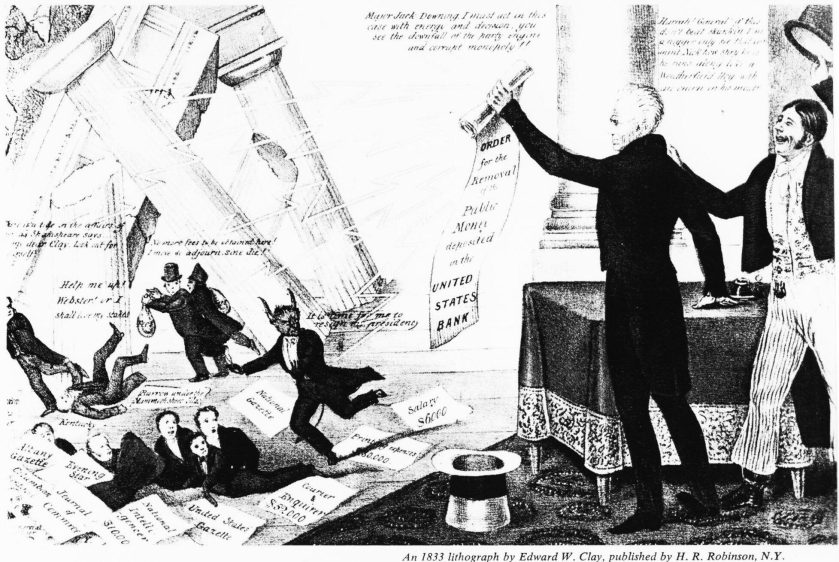

In 1803, the USA doubled in size through a land deal between the United States and France, in which the U.S. acquired approximately 827,000 square miles of land west of the Mississippi River for $15 million. Known as The Louisiana Purchase, this deal was more than the country could afford even at the bargain price of 3¢ per acre, yet it was also an offer that then president Thomas Jefferson could not refuse. The purchase deal had to be paid immediately because Napoleon needed the funds for a war with Great Britain. As a result the US was forced to borrow the funds from two banks in Europe at 6 per cent interest. It took twenty years to pay back the loan, and cost $8 million in interest fees. Even after the repayment of the loan in 1823, the USA remained in debt for another twelve years. On January 1, 1835, president Andrew Jackson paid off the entire national debt. That was the only time in U.S. history that had been accomplished.

Most nations have national or sovereign debts, and there is nothing wrong with having a debt in many cases. Most creditors don’t worry until the sovereign debt is more than 77 percent of GDP, according to the World Bank. In the fourth quarter of 2018, the U.S. debt-to-GDP ratio was 105 percent. That’s the $21.974 trillion U.S. debt as of December 31, 2018, divided by the $20.891 trillion nominal GDP. So the USA is in ‘the danger zone’ where creditors could begin panicking. This was one of the reason we lost our historical AAA+ credit after the deficit doubled under the Obama administration.

The national debt is made up of a few things, and is the total of all the bonds held at the Federal Reserve. Money begins and ends with the issuing body. When certain debts are extinguished, so is the money that created them. US Federal reserve notes are based entirely upon debt having been created through the process of fractional reserve banking. In this process, bank notes are printed and then loaned out to be repaid over time with interest. Our money is not based on a gold standard, or backed by any form of precious metals. A dollar is worth a dollar because the US Federal Reserve Bank tells you that it’s worth a dollar. It is a promissory note printed on paper or stamped on a metal coin that is redeemable for an equal amount in goods and services. For all intents and purposes, a dollar is little more than an I.O.U. Since all money created has interest attached to it, the amount of debt will always exceed the amount of money in circulation.

When president Woodrow Wilson created the Federal Reserve Bank by signing the Federal Reserve Act of 1913, he created the perfect excuse of widespread spending abuse by the government. If planned government spending exceeded the federal budget, the deficit could be plugged by borrowing the funds from the Federal Reserve Bank, at interest, for the public good. As a result, the federal deficit was $25 billion by 1934, and rose to $250 billion by 1945. In 1982, the national debt reached $1 trillion for the first time. There has almost always been massive government over-spending which blew the budget. In the past fifty years, only five years have had balanced federal budgets: 1969 under President Richard Nixon; 1998, 1999 and 2000 under Bill Clinton; and 2001 under George W. Bush.

The worst example of government over-spending occurred during the two terms of the 44th president, Barack Hussein Obama II , the worst president in history. On January 20, 2009, when he was sworn in, the debt was $10.626 trillion. On January 20, 2017, when he left, it was $19.947. President Donald J. Trump has been doing his best to slow the out of control spending, and he has been making progress. It’s going to take time to repair the damage done by the previous administration.

“President Obama has almost doubled our national debt to more than $19 trillion, and growing. And yet, what do we have to show for it? Our roads and bridges are falling apart, our airports are in Third World condition, and forty-three million Americans are on food stamps.” – Donald J.Trump

The ‘I’ in Team

You earn so much in personal income each year. Your personal income is analogous to the national income from tax revenue. Your personal budget is like a small scale version of the federal budget. Think of the national debt as you would your personal credit card. It’s the excess that has been borrowed plus interest that has been charged to bridge a spending gap. If you’re still following along with me in this example, you’re smarter than the average American.

The nation’s debt limit is similar to the limit your credit card company places on your spending. But there’s one significant difference. Congress is in charge of both its spending and the debt limit. When you max-out your credit card, one of three things happens:

- You request a limit increase, so that you can continue spending more money than you can afford.

- You request an addition line of credit, so that you can continue spending more money than you can afford.

- You stop spending more money than you can afford because no one will extend you additional credit.

On February 9, 2018, President Trump signed a bill suspending the debt ceiling until March 1, 2019. As a result, the limit will be whatever level the debt is on that day. On February 11, 2019, it was $22 trillion. At that level, the U.S. Treasury estimates it will run out of money in September 2019. The debt ceiling is a limit that Congress imposes on how much debt the federal government can carry at any given time. When the ceiling is reached, the U.S. Treasury Department cannot issue any more Treasury bills, bonds, or notes. It can only pay bills as it receives tax revenues. If the revenue isn’t enough, the Treasury Secretary must choose between paying federal employee salaries, Social Security benefits, or the interest on the national debt. Congress created the debt ceiling in the Second Liberty Bond Act of 1917. In 1974, Congress created the budget process that allows it to control spending. That’s why Congress raises the debt ceiling. Congress must raise the debt ceiling so the United States doesn’t default on its debt. During the last 10 years, Congress increased the debt ceiling 10 times. It raised it four times in 2008 and 2009 alone.

In addition to the current national debt of $22 Trillion, the USA also has additional debt in the form of unfunded obligations, or future services that the country has promised to pay for years in the future. This is an estimated additional $80 trillion, but might be as high as $200 trillion according to some estimates.

According to experts, there are three possible ways to pay off the deficit:

- Raise Taxes

- Cut Spending

- Print more money

Unfortunately, each of these by themselves are all bad ideas.

Raising Taxes

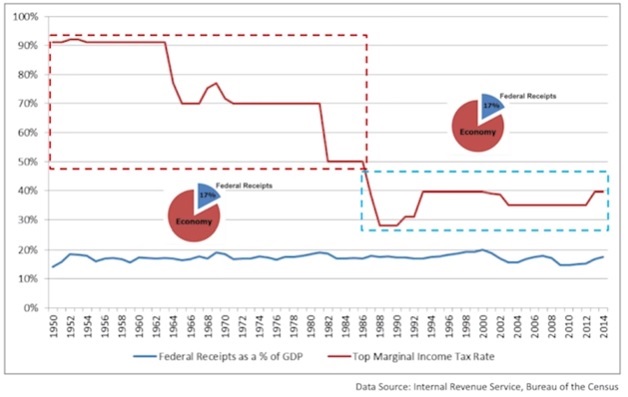

All taxes raised in this country are paid for by the top 40% of wage earners. So 60% of the workers in our country pay ZERO in federal income tax. This is why tax cuts are always tax cuts on the wealthy. It’s because only the wealthy are paying taxes, and that’s not fair. When you raise taxes on the wealthy, you stymie economic growth and slow the economy, thus reducing tax revenue. Consistently over time, the government has collected 17% in tax revenue of the total of the portion of the US economy regardless of the tax rate.

Cutting Spending

When you cut spending there are certain places you can and can’t cut, plus when you do cut some federal program, the beneficiaries of that program are going to have a hissy fit. 50% of the federal budget funds social security and medicate. So you can’t cut that. Salaries of federal employees also can’t be cut, nor can you cut military spending unless you want to weaken the defense of our nation. The only fair way to cut spending here would be to phase out certain programs, and privatize some federal jobs. The problem with privatizing some jobs is that they are tied into national security, so only cutting jobs or lowering the starting pay for new hires could reduce costs. Also this would only affect agencies that receive tax dollars to pay bills. Quasi-government agencies like the United States Postal Service would be unaffected (as they were during the recent government shutdown) because they receive no funding from tax dollars. All of their income is derived from postage sales.

Printing more money.

When you print more money, you increase the number of dollars in circulation and create inflation, so the spending power of the dollar is diminished. Also depending on how fast you increase the money supply, you run the risk of galloping or hyper inflation. Galloping inflation is when prices rise 10% each month. Hyper inflation is worse at 50% per month. Now as costs rise, salaries eventually rise to compensate, but any savings you have never increases and is worth less. Inflation is a tax on savings.

“Blessed are the young for they shall inherit the national debt.”– Herbert Hoover

Is there a way out?

According to economics professor Antony Davies there is a way to balance the federal budget within 5 years

1) Cut ALL federal spending 10% NO EXCEPTIONS.

2) Maintain this spending level for 4 years, no increases, and no adjustments for inflation.

At the end of 5 years the budget will be balanced.

If you keep the budget balanced and maintain that fixed level, eventually the economy will grow and the deficit will be paid off in about 80 years. There are ways to do it faster. The federal government collects $3.3 trillion in revenue and spends $4.3 trillion. So a straightforward way to pay off the debt would be to increase taxes 20% and cut spending 20% to run a $1 trillion surplus. That would pay off the nominal debt in about 15 years, depending on economic growth and interest rates. Unfortunately both of these seem unlikely. It is still possible to accomplish, but pie-in-the-sky programs like the Green New Deal proposed by Alexandria Ocasio-Cortez would destroy our economy, as would an expansion of the welfare state, or any move towards socialism. The best way to increase tax revenue would be through a fair tax or flat tax in which EVERY working person pays an EQUAL percentage tax, with no possible deductions or exemptions. Such a tax would drastically raise the taxes on the poorest citizens while dramatically lowering the taxes on the richest. You could also eliminate the IRS, and reduce government oversight and expenses related to tax collection and processing. Everyone would pay their fair 10%. In any case, right now we have the right man for the job sitting behind his desk at 1600 Pennsylvania Ave, Washington D.C., working overtime to Make America Great Again! As always, I wish you success and happiness!