Is there ‘too much month at the end of the money’?

The wise have wealth and luxury, but fools spend whatever they get. – Proverbs 21:20 New Living Translation (NLT)

If you’ve been paying attention so far, I’ve already touched on the importance of having an emergency fund and avoiding credit card debt in earlier blog posts. There is a reason for these two steps being essential as part of any successful plan to get out of debt. An increasing percentage of the populace lives paycheck to paycheck, lacking an emergency fund, and using credit cards to fill in the gap. This is a recipe for disaster. You cannot spend your way into prosperity. The first thing you need to understand is that you and you alone are in control of your finances. The responsibility belongs to you alone, and if you have chosen to shirk this responsibility your finances will be in total chaos. Now is the time to take action and learn to budget.

What is a budget?

A budget is a saving plan. It is not ‘punishment’, but if your finances are out of control and you’re living beyond your means, you will need to budget very tightly and stick to the plan to break the cycle of debt that you have fallen into. The good news is that it is possible. The bad news is that it will take time and effort, but I promise that if you do the work, it will pay off in the end.

Extra means extra!

Does your job pay enough for you to live on? Your paycheck is your biggest source of wealth. Social welfare programs trap you at the poverty level by doling out a meager subsistence and they should be avoided as a main source of income, preferably avoided altogether . Likewise, extra money earned from a second job, or from working overtime should not be essential to make ends meet. If you are starting out in a position of debt, you will need to increase your regular income stream in addition to budgeting. Trust me, I know from experience. Due to a series of unfortunate events from December of 1999 through January of 2002, I ended up $50,000 in debt, and it took 8 years of budgeting and working all the overtime I could endure to erase that mess. Overtime was extra income, earmarked for the specific purpose of eliminating my debt. It was never considered part of my regular monthly expenses. I have too many coworkers who have trapped themselves into working mandatory overtime just to make their monthly expenses. This is a terrible way to live.

Step one : Analyze

Do you get paid on Friday, only to be broke on Monday, wondering where your paycheck went? Successful people work from a list and write things down. Get into the habit of tracking your spending, because you’re spending way more than you realize. Write down everything you spend, and always ask for a receipt. If a receipt is not available, (like buying a soda from a vending machine) jot down a quick note and create your own receipt. Organize your receipts and record them in a journal of some sort listing the date, the store, the purchase, the amount, and the method of payment. You don’t need a fancy financial ledger for this purpose, I recommend a spiral-bound notebook. I buy these on sale at my local Wal-Mart during the back-to-school sales by the dozen, usually for the low price of just 25¢ each! Track your spending for about at least a month or two to get an accurate account of where your money goes. After this initial period, continue tracking your spending to see how it lines up with your budget.

Step two : Categorize

After you’ve collected your initial spending data break it down into categories.

Suggested categories and percentages are :

- Living expenses 50% total– Housing 25 to 35%, Utilities 5 to 15% (heat, light, phone, maybe internet and cable but those last two are questionable necessities ), Groceries 5%-15%, Transportation 5 to 10% (Bus/train fare, or parking fees, tolls if any, and gas.) You’ll need to adjust those four sub-categories based on your individual circumstances. The combined total cannot exceed 50% of your income.

- Savings 10%

- Charity 10%

- Dining and Entertainment 15%

- Clothing 5%

- Medical 5%

- Miscellaneous 5% (this can include gifts, shopping, or anything out of the ordinary)

Step three: Organize

A great way to organize your spending categories is to use the envelope system. Divide your cash into the various categories using the suggested percentages. This is all the allotment for each category. When the envelope is empty, you have no money for that expense. If at the end of the month there is unused money in any envelope, put it into an EXTRA CASH envelope, and save this for emergencies.

Step four: Follow the rules

- First rule of Budgeting – 50% of your income MUST be able to cover 100% of your living expenses. This is absolutely essential! If you get paid bi-weekly like most people, you average 2 paychecks a month, and one of those paychecks should be able to fully cover your rent, utilities, groceries, transportation, medicines etc. If you can’t achieve this with your level of income, I’m sorry to say you’ll need to find a better paying job, or cheaper living accommodations. Living in your parent’s basement forever is not a viable option either. You need to stand on your own two feet. Man up!

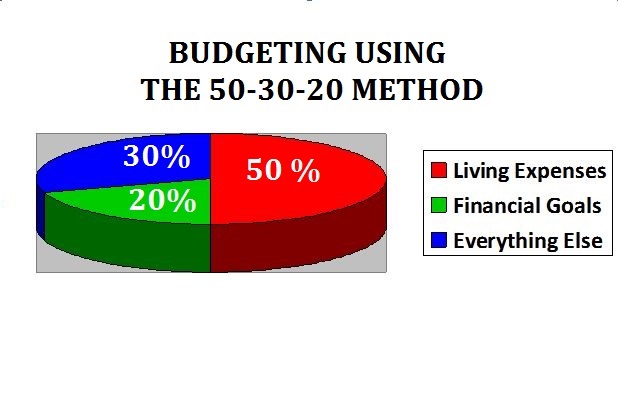

- Second Rule – The remaining 50% of your income should be as 20% Financial (savings and charity) and 30% Everything Else (dining, entertainment, misc.)

- Third Rule – Did you notice I didn’t include contributions to a 401k Retirement Plan in the two rules? That’s because you should be contributing 10% of your salary to one automatically BEFORE you even get your paycheck, and this should never ever be thought of as part of your budget. You don’t consider any other payroll deductions like taxes or FICA as part of your budget, and you should likewise think of a 401k contribution as just another in the list of payroll deductions to your check before you even get paid. If you don’t plan for your future, you won’t have one!

Cash is King!

Get into the habit of paying cash for everything! Credit cards are a tool, and can even offer benefits like cash back, but it’s way too easy to overspend and blow your budget due to impulse spending. Using cash creates a visceral reaction that credit cards lack. You really weigh your spending decisions when you leave through the dwindling banknotes in your wallet. If you elect to use credit cards for payment, you should be fully prepared to pay the balance in full each month. Paying interest is like throwing away money. If you lack the discipline to keep your spending in check, eliminate the temptation and get rid of those cards now! You’ll be happier in the long run. As always I wish you happiness and success!

What a great post on Budgeting! And congratulations on paying off $50,000 in debt!

My husband and I are currently in the process of paying of $70,000 (mostly student loans). We use the cash envelope system too. I find that it’s harder to part with cash than to swipe a debit card. It helps that you can actually see your balance getting smaller.

One thing we like to do is take any change in our envelopes at the end of the week and empty it into a jar. Once the jar is full, we cash in the change and make an extra debt payment.

LikeLike