Making reward cards, introductory rates and points work for you.

“A penny saved is a penny earned.” – attributed to Benjamin Franklin

I walk a lot outside during the day. It’s rare that a day goes by where I don’t find at least a penny on the ground. On average, I find about a dollar in coins a week, and I still stop to pick them up. When I was younger, there used to be a joke circulating about Bill Gates, (who is still one of the three richest men in the world). It ran along the lines of this: “If you average out all the money Bill Gates makes in a single year, he earns over $500 a second. If he was walking down the street and found a $100 bill lying on the ground, it would cost him money to stop and pick it up.” The most amount of money I’ve ever found lying on the ground at one time was a loose $50 bill half-buried in the snow on Liberty Ave. That was a long time ago, and I was amazed and shocked at my good fortune, but also I felt a little bad for whomever had carelessly lost that much money.

At a certain point, picking up discarded coins in the street becomes more trouble than it’s worth to some people, but I’m still of the mind-set that every penny saved adds up. To that end, I still use coupons and reward cards when I shop. These are great ways to save a few cents or even a few dollars each time you used them, and over the course of a year that can add up to hundreds of dollars.

The Store Loyalty Reward Card

Using a store loyalty reward card is easy enough, you just have to swipe or scan the card each time you shop. My local grocery store also sells gasoline (petro). At least 3 to 4 times a year, I accumulate enough points to earn a 100% discount on fuel. Gas in the USA isn’t as expensive as it is in other countries, but it’s still a fantastic savings in my book. Just always make sure when collecting point to check if and when they expire, or you may lose them with noting to show.

Reward Credit Cards

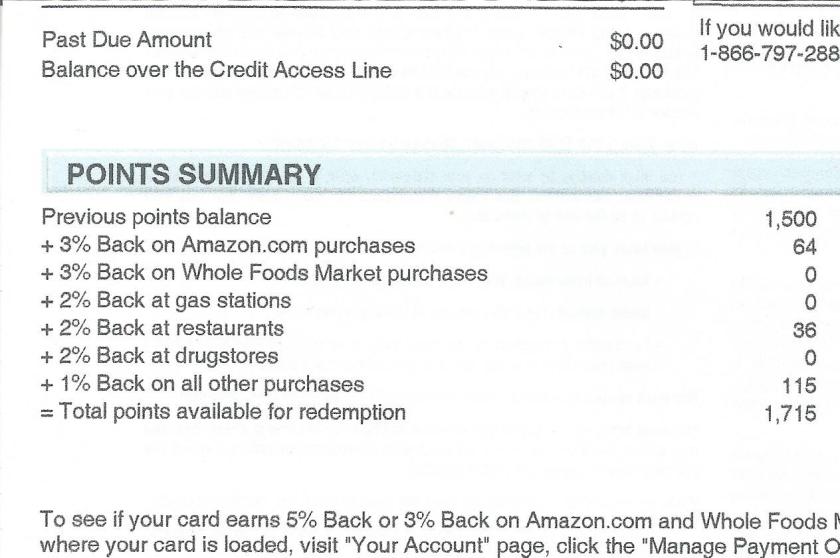

Some credit cards have a point reward system as well. These can be as simple as 1% cash back on all purchases, to a range of categories which each have a special point rating. Reward credit cards ONLY work for people with perfect credit and who pay their entire balance in full each month. The reason for this is twofold.

- You usually only receive these special offers if you have good credit. The better your FICO score, the better the offers you receive from credit card companies.

- Failing to pay the balance in full each month will cost you interest fees which will negate any savings earned by rewards.

I once read a post online where a woman was complaining about how her reward credit card was worthless because she was being charged all these fees each month for interest, exceeding her limit, and late fees. Usually the problem is not with the card, it’s user error indicative of a much greater personal problem. Never give a loaded gun to a baby, or a credit card to a fool.

Special Rates or Introductory Offers

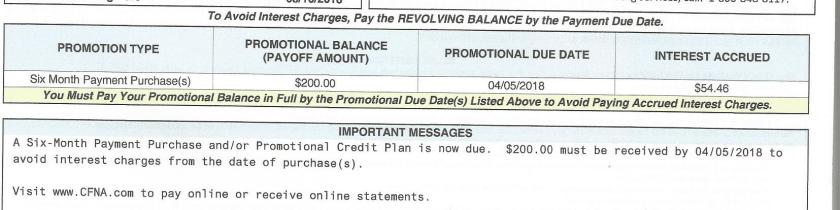

Another offer reserved for those with stellar credit are cards that offer 0% interest, fees, and balance transfers. There are great during the introductory period, BUT you must exercise extreme caution with these cards. In essence, you are playing with other people’s money. The issuing bank is allowing you to ‘play with their money’ with no fees, in the hopes that you will ring up a huge balance and not be able to pay the balance in full at the end of the promotional offer. People who lack self-control fall victim to this all the time. Interest is calculated from the time of the purchase. If at the end of the promotional period, a balance is remaining, you will incur the full interest charge of the purchase, even if you have a relatively small portion remaining. For instance: Every October, I take my car in for its annual maintenance inspection. I get all the little issues resolved, buy new tires, replace worn parts etc. Till it’s all said and done, the bill for keeping my car running another year can range from $500 to $2000. I usually pay with my Firestone Store Credit Card. It has a six months same-as-cash special promotion rate for all purchases over $299. Although the minimum monthly payment is about $20, you’ll never be able to pay the balance off in time if you only pay the minimum. The key to these cards is to divide the balance into five equal amounts, and pay that amount each month for 5 months. This allows you ONE extra month in case you need it. In the image shown below, the six-month promotion ends April 5th. Even though I’ve paid almost the full balance except for a measly $200, if I fail to send the full balance in by the due date, I will incur $54.46 in retro-active interest fees! No thanks! I (almost) never pay interest.

If you are able to take advantage of special offers like the ones I covered, enjoy yourself but always remember:

- Pay your balances in full each month.

- Pay your bill early.

- Never skip a payment, or pay the bill late.

- Never spend more money than you can afford to pay back.

As always, I wish you happiness and success!