Shh…It’s a SECRET!

This is part 2 of a 2 part series, for part one read The Big Picture!

“Whatever you believe with feeling becomes your reality.” – Brian Tracy

“Keep watching the skies!” It’s the last line spoken in the 1951 Science Fiction movie “The Thing from Another World” based on John W. Campbell Jr.’s novella Who Goes There? There are many types of conspiracy theories ranging from the ludicrous tales of UFOs and alien abductions, to countless government cover-ups. I don’t subscribe to many conspiracy theories for the simple reason that most of them are just so ‘out-there’. The few that I do occasionally look into are the more plausible ones involving ‘secret societies’ hell-bent on world domination. I’m not saying that they are true, but they are possible, albeit improbable. All conspiracy theories contain some elements of truth, even if it’s just a place, a time, people involved, and circumstantial evidence. You can take these ‘facts’ and attempt to extrapolate a bigger picture, but good luck proving it. Feelings are not facts. You can also weave the real elements into a smear campaign which is little more than a web of lies. Rather than examining the web, perhaps it’s more prudent to examine who’s spinning those webs, and who’s pulling the strings.

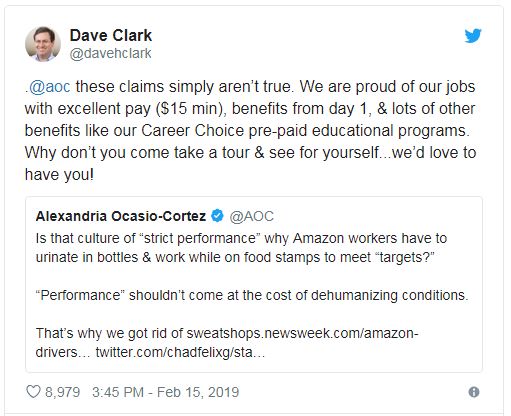

For the past two years, the left has tried in vain to show Russian collusion involving President Trump and the 2016 election results. Ever since he was elected President, Donald J. Trump has been under attack by various media outlets, entertainers, the Democrats, certain RINO Republicans, and other ‘Never Trumpers’. There has never been a greater number of outspoken domestic enemies within the government ceaselessly attempting to unseat a duly elected American president. Even his loyal supporters have been demonized, referred to as racists, Nazis, hicks, misogynists, and just plain hateful. Actress Alyssa Milano called the red MAGA hat the new Ku Klux Klan hood. Singer Madonna said she wanted to bomb the White House while wearing a pussycat hat at the so-called Women’s March in DC. At the same march, female Trump Supporters including a little girl wearing a red MAGA hat were kicked out and told they didn’t belong by radical feminists, some wearing vagina hats. Comedian Kathy Griffith destroyed her pathetic career when she thought it was ‘funny’ to pose for a picture holding a bloody severed head of Trump. She then said Trump ‘broke her’, so HER poor choice was HIS fault. The list goes on. The hatred from leftist loons knows no bounds, yet supporters of Donald Trump are branded as hate-filled ,and ridiculed. Have you ever stopped and wondered why this is? Someone, somewhere is lying to you, and manipulating the truth. A key tactic in hiding the truth when it is uncovered is to discredit the witness. The more foolish or mentally unstable that you can paint the person, the more people with little knowledge of the issues will dismiss the statements of the witness as being nothing but the ravings of a madman. Examine the facts for yourself and draw your own conclusions. Being paranoid doesn’t mean someone’s NOT out to get YOU.

“Whatever we expect with confidence becomes our own self-fulfilling prophecy.”– Brian Tracy

The truth is out there!

Since the invention of the internet, and the subsequent creation of the ubiquitous smart-phone, searching the web for any bit of information has never been easier. The few remaining holdouts that refuse to have a cell home usually still have a computer or at the very least, access to one. Society has never been more connected, and the access to the sum total of human knowledge has never been easier. If a person is determined to believe falsehoods, no amount of truth will dissuade them.

“The death of America is a real possibility. There are very powerful people in America who are working overtime to kill America”– Dinesh D’Souza Death of a Nation

Politics, economics, and religion.

The three big no-no’s of polite conversation are finances, politics, and religion. As I’ve stated before all three are interconnected to form a big picture. If you don’t understand the microeconomics of paying your own bills, and handling your own money, how can you possibly understand the macroeconomics of government finances? Worse yet, if you don’t understand the attempts of social engineering, the damaging effects of socialism, and the attempts by liberals to create ‘freedom from religion’ by banishing Christianity, you’re going to elect officials who will destroy the American Dream for every citizen, and the America created by our Founding Fathers will cease to exist.

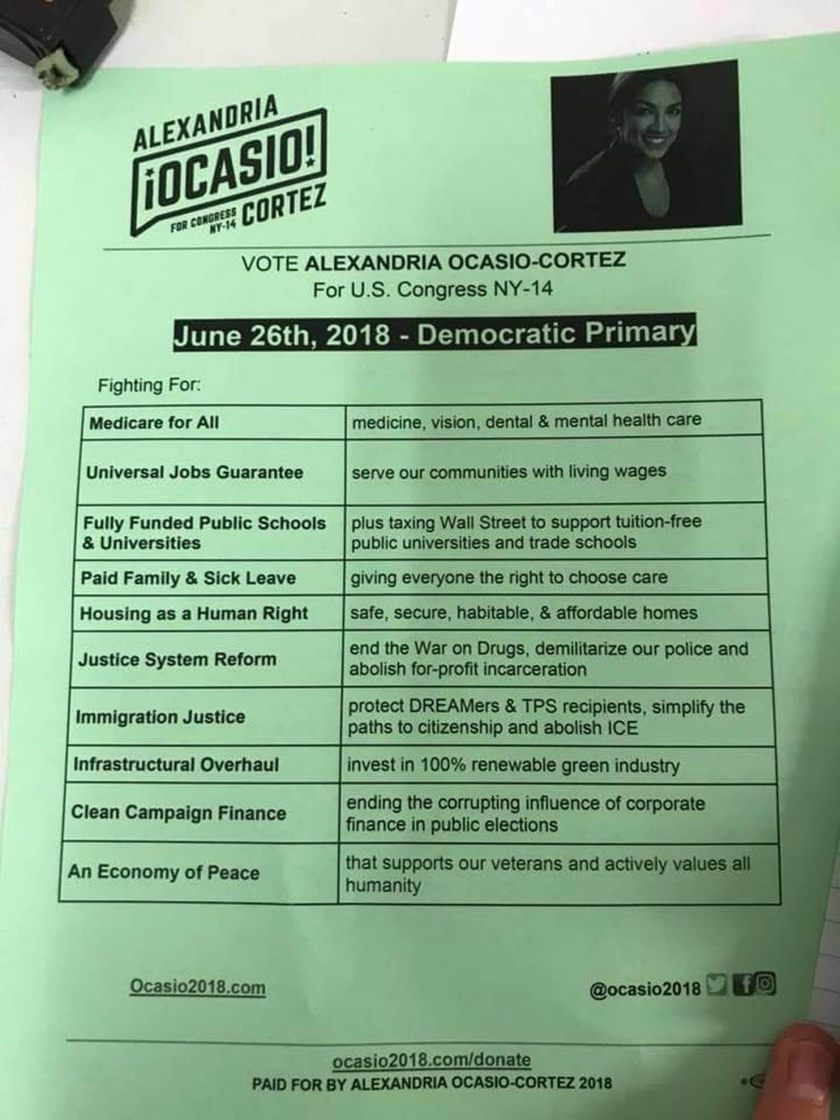

One tactic of so-called Democratic Socialists like Alexandria Ocasio-Cortez has been to sow the seeds of class warfare by alleging that world-wide poverty is the results of the many billionaires, and even millionaires who have somehow ‘stolen’ all the wealth out of greed. They want to punish successful people for becoming wealthy by imposing a tax on the highest earners of 71%. The fact still remains that the USA is 25 TRILLION DOLLARS in debt! The total amount of tax money collected from all sources cannot even begin to pay the interest on the debts we as a nation currently owe, and increasing government spending for a ‘Green New Deal’ is the worst possible idea imaginable. The welfare state needs to end. A person who chooses to be stupid and lazy has no one to blame but themselves for their deplorable condition. I don’t care if you call yourself a socialist, a libertarian, a democrat or ‘little bunny fufu’, if you’re not pro America, you’re nothing but a dirty commie!

“If destruction be our lot we must ourselves be its author and finisher. As a nation of freemen we must live through all time or die by suicide.”– Abraham Lincoln

Who’s REALLY in charge?

There are 195 countries in the world today, and of course, each one has a leader. The USA is the ‘world leader’ in terms of freedom, opportunity, and technological advances. We are the longest lasting constitutional republic in the history of the world. Not ‘every’ nation in the world likes us, but the majority do.

Up until the eighteenth century, leadership of a nation was the greatest goal a person could achieve. That has changed in the past two centuries. Captains of industry have become the modern day ‘kings’ of the world, with world domination being a ‘game of kings’

The Illuminati is a name given to several groups, both real and fictitious. Originally, the Illuminati were a secret society created in 1776. Other such secret societies include the Freemasons and The Skull and Bones Society. According to some conspiracy theorists, these and subsequent subgroups are hell-bent on world domination, and the only thing standing in their way is the USA. It’s an interesting theory, and impossible to prove, or disprove. How does this affect the average person? If total control of the world is inevitable, you absolutely positively want to have the most benevolent world leader. The average person has no real control, so worrying about such things will not change a thing. Eventually, nations die because of despotism, decadence, and debauchery, so it’s important to keep our nation strong. The USA is a republic. We elect officials to enact laws on our behalf. Essentially we are handing over control of our lives to leadership who have the power to enact laws that will affect us, our children, and our children’s children. The best defense against bad government policy is a well-educated public. As Former president Ronald Reagan once said, “Man is not free unless government is limited,” and, “Freedom is never more than one generation away from extinction.”

“The fundamental question of our time is whether the West has the will to survive. Do we have the confidence in our values to defend them at any cost? Do we have enough respect for our citizens to protect our borders? Do we have the desire and the courage to preserve our civilization in the face of those who would subvert and destroy it?” – President Donald J. Trump quote from speech in Warsaw Poland July 6th 2017

Q and The Plan to save America

As I stated previously, secret societies have existed for centuries. IF one were to ‘guess’ the membership of these groups the wealthiest people in the world would ‘probably’ number among them, as would many world leaders. According to legend, the Illuminati is comprised of a Committee of 300 of the most powerful and influential people in the world. These would PROBABLY be people who have seized power and held on to it for a very long time. They would also, probably have their hands in the Trilateral Commission (established by Jimmy Carter, Zbigniew Brzezinski, and David Rockefeller in 1973) and most assuredly meet at the ultra-secretive Bilderberg Meeting , an annual conference established in 1954 by Prince Bernhard of the Netherlands “to foster dialogue between Europe and North America”. There are entire books written on all of these groups if you want to research them further. The bottom line is that globalism spells the death of nationalism.

Donald J. Trump was a Washington outsider who for over 30 years stated again and again that he would only seriously run for president IF he felt that our nation was in danger of being destroyed by those who wish to ‘extinguish the light of Liberty’. President Trump is a true patriot, and he is actively repealing the destructive legislation enacted by previous administrations. He is hated by liberals because he really wants to Make America Great Again and believes in the American dream.

The amazing side effect of having the sum total of human knowledge at our fingertips, and the fact that we are more ‘connected’ than ever is that many of these secrets and lies have been exposed through crowd-sourcing and social bookmarking. we are witnessing right now one of the greatest communications events in history. I am referring to the Q anon phenomenon. Call this if you will, a ‘reverse’ secret society.

On October 28, 2017, an anonymous person identifying as “Q Clearance Patriot” first appeared on the /pol/ board of 4chan, an anonymous online community. The Q clearance refers to a United States Department of Energy security clearance required for access to Top Secret information about nuclear weapons and materials. There is no way to track the identity of a 4chan or 8chan user. Some people have theorized that this is a group of either government patriots with high ranking military ties, or a hoax perpetuated by hackers and online trolls. Some of the evidence texted by Q, sometimes called Q drops, or Q crumbs, hint that a group of powerful patriots begged Donald Trump to finally throw his hat in the ring for president in the last, best attempt to battle the deep state and corrupt media intent on destroying this country. Many of the facts presented are eye-opening, and more often than not Q encourages his followers to follow the white rabbit and do their research, often asking questions in order to encourage cognitive thinking and civil discourse. If you’ve seen disturbing images shared on social media like Facebook or Twitter, I strongly advise avoiding 4chan or 8chan. These are the ‘wild west’ sections of the internet, anything goes, and some online trolls like to post some very nasty things in the comments to some of the Q Crumbs. The basic message in a nutshell is that Donald Trump is a great man, and that the media is attempting to destroy him using vicious lies, such as Russian collusion and mental instability. Because of the freedom of information shared through the internet, these lies have been exposed. A storm is coming, and America will be saved from those who wish to destroy it.

Many of the search hashtags used include #WhereWeGo1WeGoAll #WWG1WGA #QAnon #Q

If you are interested in researching Q further, you can search through the Q drops and replies on https://qmap.pub/ and https://qanon.pub/ Again, be aware that there might be things that you don’t want to see mixed in with the must see and must read stuff.

The REAL Bottom Line!

Again Jesus spoke to them, saying, “I am the light of the world. Whoever follows me will not walk in darkness, but will have the light of life.” John 8:12

Anything shrouded in darkness and secrecy is not good. Jesus is light of the world and the King of kings. People who chose to ignore this have slandered, despised, and ridiculed Christ since the first century. The Bible tells us that one day all of this world will be swept away in a great battle between the forces of good and evil. When that day arrives, those on the side of evil will face judgment for their sins. The Bible is the ONLY truth on Earth you will ever read. If there was ONE source of information I would implore you to search more than any other, The Bible would be it. Our Founding Fathers were Christians, this nation was founded as a Christian nation. There have been many people throughout the past 243 years who have sided against the USA. Everyone of them has failed in the end. Don’t worry, God’s got this fight in the bag. Until that final day of Judgment, elect moral leadership every chance you can, because if your aren’t serving the King of kings, I hope you like very warm temperatures. As always, I wish you success and happiness!